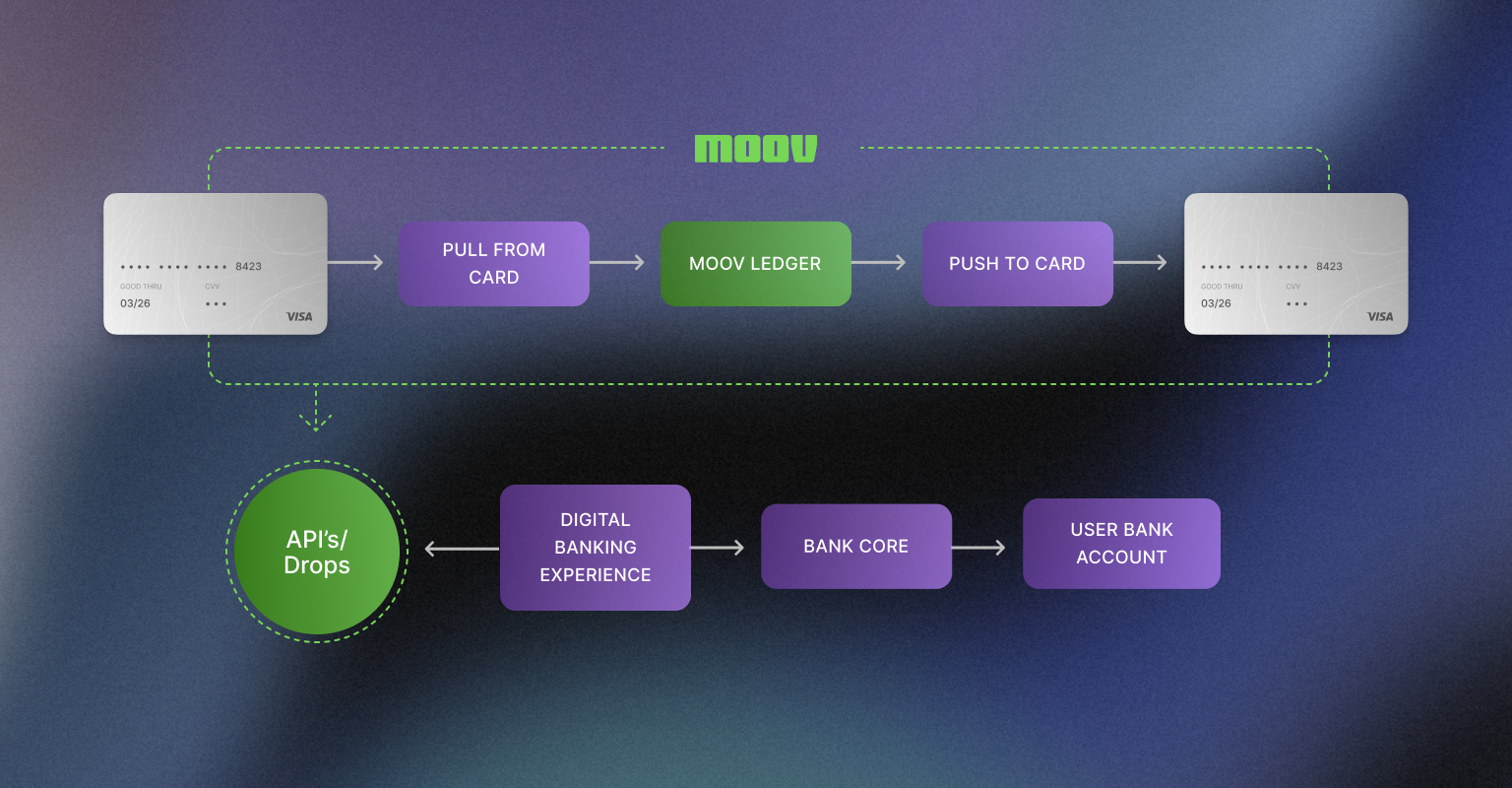

How Moov enables easy push and pull card payments

Instant is becoming the new standard for virtually everything—including money movement. And it’s not just a matter of convenience. The ability to transfer and access funds in near-real time, 24/7/365, can solve cash flow challenges and open up new payments use cases and business models.

While instant payments are still in their infancy in the U.S., the category is growing fast both domestically and across the globe. Case in point, instant payment solution Visa Direct has seen consistent growth in recent quarters, showing roughly 20% year-over-year increases, with their revenue around new payment flows up 17%. And, according to Juniper Research, instant payments volume will more than double in the next 3 years. They predict that total instant payments will jump from 74 billion to 235 billion transactions globally and that almost 70% of all consumer payments will be instant.

Those numbers are huge! And they represent an opportunity that FIs should take full advantage of by offering a full array of instant payment options—from RTP (Real Time Payments) to the topics of today’s discussion: card-based instant transfers, specifically pull from card and push to debit transactions.

Despite the immense benefits of these payment options, many financial institutions have yet to adopt them. This article will briefly describe both pull from card and push to debit payments, explain their value, and share how Moov can help FIs offer them easily.

What are pull from card transactions?

A pull from card transaction occurs when a bank debits funds from a cardholder’s account to fund a different account—in fact, some providers refer to them as account funding transfers (AFTs), because it’s exactly what they do. As the “pull” implies, the bank or payment provider pulls the funds from the cardholder’s account, instead of the cardholder initiating the transfer—though the cardholder does grant permission.

Common examples include:

- Funding a digital wallet

- Moving money into a checking or savings account

- Adding funds to a prepaid card account

- Funding a P2P transfer

What are push to debit transactions?

Push to debit transactions are real-time payments that transfer funds directly from a business’s bank account or digital wallet to a cardholder’s. They are, in many ways, the inverse of a pull transaction—funds are “pushed” directly to the recipient’s account—just like a refund you get when returning something to Amazon. These are sometimes called OCTs, (original credit transactions) because there’s no previous transaction being refunded; the credit is the original transaction. Networks love to leverage legacy technology for novel flows all the time!

There are a lot of use cases for push to debit. The most obvious use is to simply carry out the opposite of the pull from card examples above (funding wallets, etc.)—instantly pushing money out of one account into another. An example most of us are familiar with is cashing out your Venmo balance in real time.

There are a ton of other business applications as well, including:

- Commission payouts or corporate expense reimbursements

- The purchase of digital goods within games or online marketplaces

- Gig worker, shared economy, and tip payouts

- Rebates or reimbursement of overpayment

- Disbursements of loans or insurance payouts

- Education disbursements

- Security deposit refunds

- Refunds due to bad customer experiences

Why should banks offer pull from card and push to debit transactions?

There are obvious competitive advantages for financial institutions that have decided to offer card-based instant payments, such as:

Engagement

Convenience and speed matter. Most people have quicker access to their debit card info than their checking account numbers; giving them the option to quickly use the card they have close at hand helps keep them engaged. It also provides you with opportunities for new fee revenue that the market has proven consumers are willing to pay for. And the ability to move money instantly at any time, 24/7/365, opens up countless opportunities for engagement. Banking isn’t as sticky as it used to be. Consumers will only say, “My bank doesn’t do X” so many times before shopping for a new alternative.

Deposit growth

No one wants to see consumer accounts, already a cost center, sitting idle; faster funding reduces the chances of this happening. By enabling customers to instantly move money from external sources as they set up the account, you’ll gain deposits on day one and have a greater chance of gaining primary FI status.

Loans, lines of credit, and revolving accounts

Card-based instant transfers create a better experience whether you’re originating or servicing a loan. When originating, you can make funds instantly available when and where the borrower needs them; when servicing, you can allow customers to fund their associated account more easily to pay their balances.

Why do so few banks offer pull from card and push to debit transactions?

Most banks understand the benefits of card-based instant payments, but are unable to offer them for various reasons. In my experience, these are the most common:

Partnership and ecosystem complexities

To put together a card acquiring program, you need, at minimum, a strong Acquiring Bank, a processor, a ledger to clear and reconcile all the inbound and outbound payments to the bank, and multiple network relationships. Each of these entities has specific requirements and associated costs. For most banks, the investment feels too large.

Lack of expertise

While banks, digital payments providers, and core banking solutions have been running debit card programs and partnerships for decades, card acquiring has been limited to agent bank referral relationships for business clients. So there’s little institutional knowledge, no existing integrations, and a limited network of partnerships.

Hiring burden

To address all of the necessary expertise and partnership requirements, FIs need to build out their internal expertise and infrastructure. They’ll need resources to:

- Develop and manage the new partnerships.

- Manage funding flows and reconciliation resources.

- Build and maintain network connections. This includes managing the differences in settlement windows, rules, and limits across various networks.

- Create and implement fraud and risk policies specific to their new flows and infrastructure—and keep it up to date with the ever-changing requirements of an evolving payments landscape.

Most financial institutions have enough on their plates without taking on these additional tasks. The good news is that they don’t have to take them on. Moov can help.

How can Moov help?

Moov solves the above challenges through a new kind of infrastructure. We’re not just another piece of middleware or a layer of abstraction on top of existing infrastructure. Our unique architecture provides a direct, single point of integration to all major card networks.

Here’s how our infrastructure allows us to support FIs’ use of card-based instant transfers:

One-to-many partner management

Offering card-based push and pull payments would require you, at the very minimum, to build relationships with Visa and MasterCard—plus, potentially, an additional sponsor bank to handle the card acquiring aspects of instant transfers. But partnering with Moov puts you into seamless partnership with multiple payment rails. We’ve built the relationships and done the heavy lifting, so you don’t have to.

Synchronized settlement

Moov attacks payments infrastructure with a reconciliation-first approach. We handle all network settlement, clearing transfers each step of the way—from initial transaction to settlement via our real-time, dual-entry ledger. And as a single point of integration, we can offer a single source of truth to make reconciliation quick and easy.

Synchronized rules and limits

From a distance, card brands appear pretty similar, but they have some very specific differences—including significant distinctions in the rules and limits associated with instant transfers. Moov manages and keeps up to date with these rules to ensure program compliance from both network and regulatory perspectives.

Specialized fraud prevention

A lot of FIs believe instant transfers and fraud go hand in hand, but this isn’t necessarily the case. Moov has the depth and breadth of expertise and the network capabilities to provide an effective, targeted approach to fraud mitigation. We perform ongoing transaction monitoring to detect trends and potential misuse. We also employ best-in-class KYC, ANI (Account Name Inquiry), and AVS (Address Verification Service) processes to ensure the cards involved in these transfers belong to the appropriate account holder.

Simple integration

Fast and easy integration is key to Moov’s value. We’re built to be a single core integration and set of agreements, as well as one source of truth for all your money movement. We offer simple hosted onboarding for FIs, and our payments experiences can be easily customized with our modular UI elements called Moov Drops.

Learn more

Want to offer payment options that are fast, convenient, and meet the growing number of use cases and opportunities emerging across the payments space? Moov can help. We make it more than possible to offer instant push and pull payments—we make it easy.

Reach out today to learn more.